KARACHI:

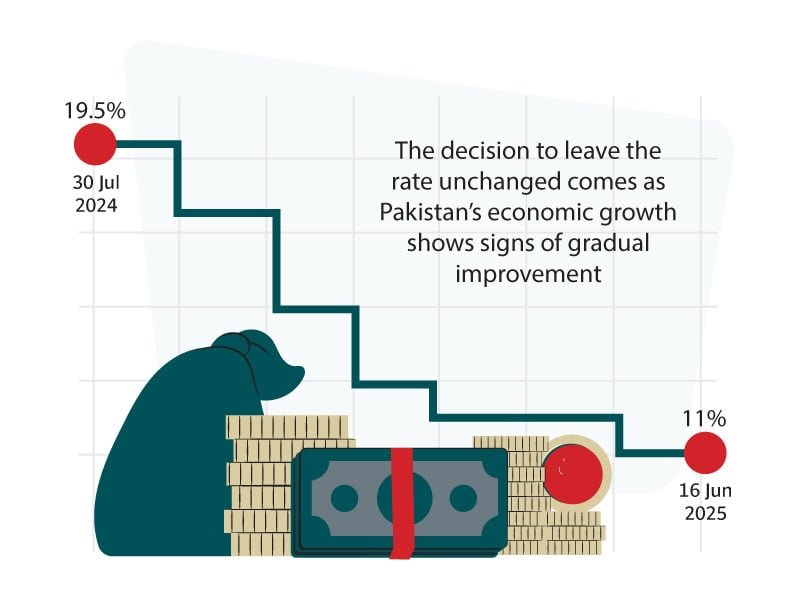

The State Bank of Pakistan’s Monetary Policy Committee (MPC) on Monday decided to keep the policy rate unchanged at 11%, as it cautiously navigates multiple economic challenges. While inflation expectations remain contained for now, the central bank flagged rising risks to the external sector due to a widening trade deficit, weak financial inflows, and global uncertainties including volatile oil prices and geopolitical tensions. Domestically, the economy faces subdued agricultural output, heavy reliance on domestic borrowing, and the pressing need for structural reforms, including broadening the tax base and privatising loss-making public enterprises, to ensure fiscal consolidation and sustainable growth.

In its latest review, the MPC noted that the year-on-year headline inflation rose to 3.5% in May 2025largely as anticipatedcompared to 0.3% in April. However, core inflation saw a marginal decline, and inflation expectations among businesses and households also moderated. The committee maintained that inflation is expected to trend higher in the coming months but will likely stabilise within the target range of 5% to 7% during fiscal year 2025-26 (FY26).

The decision to leave the policy rate unchanged comes as Pakistan’s economic growth shows signs of gradual improvement. The real GDP growth for the outgoing fiscal year is provisionally estimated at 2.7%, with the government targeting an ambitious 4.2% growth for FY26. The MPC expects the impact of prior interest rate cuts to continue filtering through the economy, further boosting demand and investment activity over the next year.

Despite these positive signals, the committee flagged several challenges that could undermine the recovery momentum. Chief among these is the sustained widening of the trade deficit and sluggish financial inflows, which have heightened pressures on the external account. The MPC also warned that some of the proposed budgetary measures for FY26such as incentives or subsidies that could spur importsmay exacerbate the trade imbalance.

Among recent economic developments, the MPC pointed to the broadly balanced current account position in April 2025, which brought the cumulative surplus to $1.9 billion in the July-April period. This balance was supported largely by strong workers’ remittances, which helped offset the impact of rising imports and slowing exports amid a tough global trading environment. The disbursement of $1 billion under the first review of the International Monetary Fund’s Extended Fund Facility contributed to boosting the SBP’s foreign exchange reserves to $11.7 billion by early June.

However, the external outlook remains precarious. The MPC expects the current account to shift into a moderate deficit in FY26, as domestic demand leads to stronger import growth while export prospects remain dim due to persistent global economic uncertainty. Additionally, financial inflows have not met expectations, though reserves are projected to climb to $14 billion by the end of June 2025. The committee also highlighted risks stemming from geopolitical tensions, particularly in the Middle East, and volatility in international oil pricesfactors that could worsen the external sector position.

On the fiscal side, the MPC mentioned improvements in both the overall fiscal and primary balances for FY25. The primary surplus is now projected at 2.2% of GDPup from 0.9% the previous yearhelped by rising revenues and restrained expenditures, especially in public sector development programs (PSDP). For FY26, the government aims for a higher primary surplus target of 2.4% of GDP. The central bank emphasised that maintaining fiscal discipline through effective reformssuch as broadening the tax base and overhauling state-owned enterpriseswill be critical to sustaining macroeconomic stability.

Turning to the real economy, the MPC noted that GDP growth picked up pace in the second half of FY25, reaching 3.9% after a subdued first half marked by only 1.4% expansion. While industry and services sectors drove the recovery, agriculture lagged behind due to a notable drop in major crop production. The outlook for the agriculture sector remains cautious, with early data on the Kharif season suggesting potential setbacks due to unfavourable weather conditions. In contrast, momentum in industry and services is expected to continue, supported by improving business confidence, private sector credit expansion, and rising imports of machinery and intermediate goods.

In the monetary domain, broad money (M2) growth slowed to 12.6% by late May, down from 13.3% at the previous policy review. This deceleration was attributed to reduced government borrowing from the banking system. Meanwhile, private sector credit rose by 11%, reflecting robust demand from textiles, telecommunications, and wholesale and retail businesses. Consumer financing also expanded at a healthy pace, indicating improved economic sentiment.

The MPC observed a sharp rise in reserve money growth, largely driven by seasonal demand for cash during Eid. To manage liquidity and keep the interbank overnight repo rate close to the policy rate, the SBP ramped up its liquidity injections into the banking system.

Despite the modest rise in inflation in May, energy prices remained lower compared to the previous year due to the earlier decline in global oil prices. However, the central bank cautioned that recent budgetary measures could introduce near-term price volatility, though their overall inflationary impact is expected to be limited. Risks to the inflation outlook remain, including potential disruptions in global supply chains, geopolitical conflicts, commodity price swings, and adjustments in domestic energy tariffs.

#SBP #holds #interest #rate